Starting a business is one of the most exciting and rewarding journeys you can take. It represents freedom, flexibility, and the opportunity to bring your vision to life. For many entrepreneurs, it’s not just about making money, it’s about creating something meaningful, solving problems, and leaving a lasting impact.

But while the dream is powerful, the reality is often filled with challenges. The first five years of running a business can feel like a rollercoaster: long hours, tough decisions, and constant learning curves. And unfortunately, the numbers show just how tough it can be.

According to the U.S. Bureau of Labor Statistics, survival rates for new businesses decline steadily over time. Many businesses make it through the first year, but the numbers drop as the years go on.

For example, among businesses that opened in 2013, only about 34.7% were still operating 10 years later, which means nearly two-thirds had closed by 2023. Five-year survival rates for most groups typically fall in the 40% to 60% range, showing just how challenging those early years can be.

These statistics can feel discouraging, but they also highlight something important: most businesses don’t fail because the idea was bad, they fail because of preventable mistakes.

The encouraging news is that with the right preparation, mindset, and strategies, you can avoid many of the common pitfalls that trip up new entrepreneurs.

I’m Whitney, President and Founder of WG Business Enterprises, and for over 12 years I’ve worked with business owners across industries to streamline operations, strengthen leadership, and build sustainable growth strategies.

In that time, I’ve seen patterns emerge where the same mistakes are repeated over and over again by well-meaning, passionate entrepreneurs.

The good news? Once you know what to look out for, you can set your business up for long-term success.

Table of Contents

Why Many New Businesses Fail

The truth is, most failures come down to avoidable missteps rather than flawed ideas. Entrepreneurs often launch with energy and passion, but they overlook foundational steps that could protect their business in the long run.

Below, I’ll walk you through the 10 most common mistakes new businesses make in their first five years, and share quick, actionable tips you can use to avoid them.

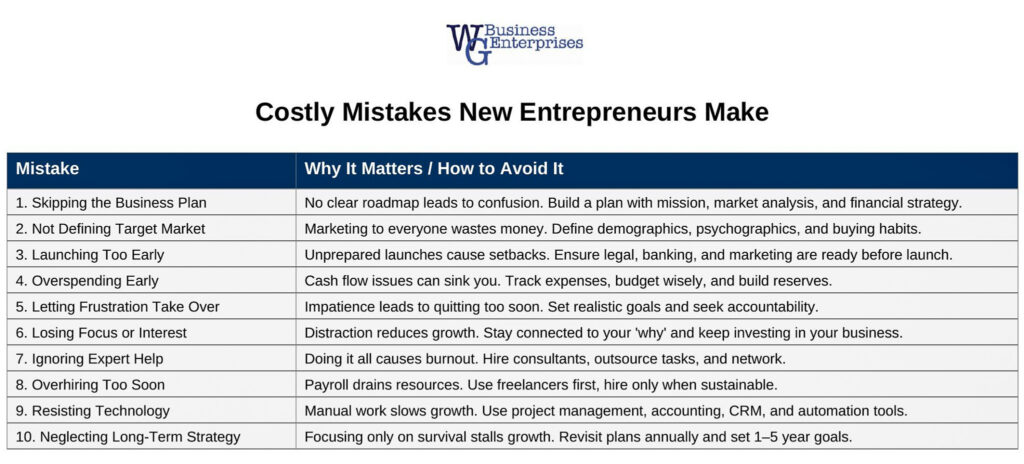

1. Skipping the Business Plan

Many entrepreneurs jump into their new venture with excitement and passion, but without a clear plan, even the best ideas can quickly unravel. A business plan is more than just a document for investors, it’s your roadmap.

It forces you to think critically about your mission, your goals, your target market, and how you’ll generate revenue. Without it, you risk making impulsive decisions, wasting resources, and losing sight of your long-term vision.

Think of it this way: you wouldn’t build a house without a blueprint, and you shouldn’t build a business without one either.

Quick Tips for a Strong Business Plan:

- Mission Statement: Define why your business exists

- Product/Service: Describe what you offer clearly

- Goals: Outline short- and long-term objectives

- Strategy: Map out how you’ll reach those goals

- Financial Plan: Budget, forecast, and funding sources

2. Not Defining Your Target Market

One of the fastest ways to burn through money and energy is trying to market to “everyone.” When you don’t know exactly who your ideal customer is, your messaging becomes vague, your marketing feels scattered, and your sales efforts lose impact.

Successful businesses understand their audience deeply. They know their demographics, their pain points, and their buying habits.

The more specific you are about who you serve, the easier it becomes to create products, services, and campaigns that resonate.

Remember: if you try to speak to everyone, you end up connecting with no one.

Quick Tips to Identify Your Market:

- Demographics: Age, gender, income, education

- Psychographics: Interests, values, and lifestyles

- Behaviors: Buying patterns and brand loyalty

- Pain Points: The problems your business solves

- Channels: Where they spend time (social media, events, etc.)

3. Launching Too Early

The thrill of starting a business often pushes entrepreneurs to launch before they’re fully prepared. While enthusiasm is important, rushing into the market without completing the necessary groundwork can backfire.

If your branding looks unfinished, your product isn’t ready, or your finances aren’t in order, you risk damaging your credibility before you’ve even had a chance to build trust.

A strong launch sets the tone for your reputation, and first impressions matter. Taking the time to prepare thoroughly ensures you start from a position of strength rather than scrambling to fix mistakes later.

Quick Tips Before Launch:

- Complete all necessary legal and government paperwork

- Open a dedicated business bank account

- Finalize your product or service offering

- Create marketing basics like a website, business cards, and social media presence

4. Overspending in the Early Stages

When the emotions of a new business are fresh, it can be tempting to spend big on things that make you feel “official”, such as a fancy office, premium software, or expensive branding.

But overspending in the early stages is a common trap that drains your most valuable resource: cash flow.

Every dollar you spend on non-essential items is a dollar you can’t invest in growth.

Successful entrepreneurs know how to keep things lean in the beginning, focusing only on what truly drives revenue. By keeping expenses under control, you give your business the breathing room it needs to survive the unpredictable ups and downs of the early years.

Quick Tips to Avoid Overspending:

- Track every single expense carefully

- Stick to a realistic budget

- Delay “nice-to-haves” until your income supports them

- Save reserves for slow or unpredictable months

5. Letting Frustration Take Over

Building a business takes time, and results rarely happen as quickly as we hope. When growth is slower than expected, frustration can creep in and cloud your judgment.

Some business owners react by making rash decisions, while others give up too soon. The truth is, sustainable success requires patience, persistence, and the ability to stay steady even when things feel uncertain.

Frustration is natural, but it shouldn’t control your actions. By managing your mindset, setting realistic expectations, and focusing on steady progress, you’ll be better equipped to ride out the tough moments and keep moving forward.

Quick Tips to Manage Frustration:

- Set realistic, measurable goals

- Reevaluate your pricing or marketing if growth stalls

- Seek mentorship, coaching, or join a mastermind group

- Focus on steady progress instead of quick wins

6. Losing Focus or Interest

Entrepreneurship is filled with distractions. New opportunities pop up, competitors shift strategies, and shiny new ideas can feel more exciting than the slow grind of building your current business.

But losing focus is one of the biggest threats to long-term success. When you constantly change direction, you dilute your efforts and confuse your customers.

The businesses that thrive are the ones led by owners who stay committed to their vision, even when the road gets tough. That doesn’t mean you can’t pivot when necessary, but it does mean staying grounded in your “why” and resisting the temptation to chase every new idea.

Quick Tips to Stay Focused:

- Revisit your “why” regularly to stay motivated

- Continually invest in skills and business improvements

- Explore new revenue streams strategically

- Stay adaptable to shifts in your industry

7. Ignoring Expert Help

Many new business owners fall into the trap of thinking they have to do everything themselves. While this do-it-all mindset can feel empowering at first, it quickly leads to burnout and costly mistakes.

No one can be an expert in every area, finance, marketing, operations, technology, and legal compliance all require specialized knowledge. By refusing to seek help, you may spend hours struggling with tasks that an expert could complete in minutes, or worse, make errors that hurt your business in the long run.

Smart entrepreneurs know that investing in guidance, whether through consultants, mentors, or outsourced professionals, is not a cost but a growth strategy.

Surrounding yourself with the right expertise allows you to focus on your strengths and accelerate your progress.

Quick Tips to Leverage Expertise:

- Hire consultants for specialized areas like finance or IT

- Outsource tasks that drain your energy and time

- Build relationships with professionals in your field

- Use platforms like LinkedIn to connect with experts

8. Overhiring Too Soon

As your business begins to grow, it’s natural to want extra hands on deck. However, hiring too many employees before your revenue can support them is a mistake that can sink your business.

Payroll is often one of the biggest expenses for small businesses, and overhiring too early can quickly drain your resources.

Beyond the financial strain, bringing on too many people too soon can also create inefficiencies, confusion, and unnecessary complexity in your operations.

The key is to scale strategically, by starting lean, make use of freelancers or contractors, and only commit to full-time staff when the workload and income consistently justify it. This approach allows you to stay flexible while still getting the help you need.

Quick Tips for Smart Hiring:

- Begin with freelancers or contractors when possible

- Develop an organizational chart with defined roles

- Only hire when workload and revenue justify it

- Prioritize positions that directly generate income

9. Resisting Technology

Technology is no longer optional for small businesses, it’s essential. Yet many entrepreneurs resist adopting new tools because they feel overwhelmed, intimidated, or stuck in old ways of doing things.

This resistance can put you at a serious disadvantage. Tools like customer relationship management (CRM) systems, accounting software, project management platforms, and automation can save you time, reduce errors, and allow you to compete with much larger companies.

By refusing to embrace technology, you risk falling behind competitors who are running more efficiently and delivering better customer experiences. The earlier you integrate the right technology, the smoother your operations will run and the more time you’ll free up to focus on growth..

Quick Tips for Using Technology:

- Use project management software to stay organized

- Adopt accounting tools to manage cash flow effectively

- Leverage a CRM system to nurture customer relationships

- Automate repetitive tasks like invoicing and social media

10. Neglecting Long-Term Strategy

In the early days of running a business, it’s easy to get caught up in the daily grind of survival, like paying bills, serving customers, and putting out fires. But if you only focus on the short term, you’ll eventually hit a ceiling.

Long-term strategy is what allows businesses to grow, adapt, and thrive beyond the startup phase. Without it, you risk stagnation or being blindsided by changes in the market.

A strong long-term plan helps you set measurable goals, anticipate challenges, and create systems that can scale with your growth. It’s not about predicting the future perfectly, but about preparing your business to evolve and seize opportunities as they arise.

It’s easy to focus on daily survival, but without a long-term plan, growth becomes stagnant. Businesses that think ahead are better positioned to adapt, scale, and seize new opportunities.

Quick Tips for Long-Term Planning:

- Revisit your business plan at least once a year

- Set 1-year, 3-year, and 5-year measurable goals

- Monitor trends and competitor strategies

- Create systems that allow scalability and flexibility

FAQs About New Business Mistakes

1. Why do most small businesses fail in the first five years?

Skipping a business plan, overspending in the early stages, or not understanding the target market are the most common pitfalls. By addressing these early on, entrepreneurs dramatically increase their chances of survival.

2. What is the biggest mistake new entrepreneurs make?

The biggest mistake is trying to do everything alone. Many entrepreneurs resist seeking expert help, outsourcing, or leveraging technology. This often leads to burnout and inefficiency. Successful business owners learn to delegate and bring in specialized expertise when needed.

3. How important is a business plan for startups?

A business plan is critical because it acts as a roadmap. It clarifies your mission, outlines your goals, and helps secure funding. Without it, you may lack direction, overspend resources, or fail to anticipate challenges. Treat it as a living document and update it regularly.

4. How can I avoid overspending when starting a business?

Start lean by focusing on essential expenses. Track every dollar, avoid unnecessary purchases, and build a financial reserve for slower months. Separate your personal and business finances to keep your cash flow healthy and transparent.

5. Should small businesses invest in technology right away?

Yes. Even at the startup stage, technology improves efficiency and saves time. Tools like project management software, accounting platforms, and customer relationship management (CRM) systems help small businesses compete with larger ones by reducing errors and improving productivity.

6. When is the right time to hire employees for a new business?

Hire when your business model can sustain it. Many entrepreneurs make the mistake of overhiring too soon, which can drain resources. Start with freelancers, contractors, or outsourcing. Only move to full-time employees once revenue and workload justify it.

Conclusion & Next Steps

Building a successful business is a marathon, not a sprint. The first five years are critical, but by avoiding these common mistakes, you dramatically increase your chances of long-term success.

Remember: every thriving business owner once stood where you are now. The difference between those who succeed and those who don’t is preparation, persistence, and a willingness to learn.

At WG Business Enterprises, we specialize in helping small and medium-sized businesses streamline operations, strengthen leadership, and grow profitably.Ready to avoid costly mistakes and accelerate growth? Schedule your free consultation today.

For more insight, explore our blog post: Why Outsourcing Project Management Helps Business Thrive.

Click the button below, and one of our consultants will reach out to you.

Serving West Palm Beach, Palm Beach County, and clients across the U.S.

Contact WG Business Enterprises for your free consultation.

Free Business Resources & E-books:

Free Guide to SMART Goals for Businesses

Free Guide to Optimizing Your Business

Free Guide to a Hassle-Free Office Move